The Reversal Indicator — Coding in Python.

Coding the Rob Booker Reversal Indicator in Python.

Some less-known indicator actually function pretty well. Among those indicator is Rob Booker’s Reversal Indicator which uses a special combination between the MACD oscillator and the Stochastic oscillator. This article discusses creating the indicator in Python. All credits go to Rob Booker.

I have just published a new book after the success of my previous one “New Technical Indicators in Python”. It features a more complete description and addition of structured trading strategies with a GitHub page dedicated to the continuously updated code. If you feel that this interests you, feel free to visit the below Amazon link, or if you prefer to buy the PDF version, you could contact me on LinkedIn.

The MACD Oscillator

The MACD is probably the second most known oscillator after the RSI. One that is heavily followed by traders. It stands for Moving Average Convergence Divergence and it is used mainly for divergences and flips. Many people also consider it a trend-following indicator but others use graphical analysis on it to find reversal points, making the MACD a versatile indicator.

How is the MACD calculated? It is the difference between the 26-period Exponential Moving Average applied to the closing price and the 12-period Exponential Moving Average also applied to the closing price. The value found after taking the difference is called the MACD line. The 9-period Exponential Moving Average of that calculation is called the MACD signal.

# The function to add a number of columns inside an array

def adder(Data, times):

for i in range(1, times + 1):

new_col = np.zeros((len(Data), 1), dtype = float)

Data = np.append(Data, new_col, axis = 1)

return Data# The function to delete a number of columns starting from an index

def deleter(Data, index, times):

for i in range(1, times + 1):

Data = np.delete(Data, index, axis = 1)

return Data

# The function to delete a number of rows from the beginning

def jump(Data, jump):

Data = Data[jump:, ]

return Data# Example of adding 3 empty columns to an array

my_ohlc_array = adder(my_ohlc_array, 3)# Example of deleting the 2 columns after the column indexed at 3

my_ohlc_array = deleter(my_ohlc_array, 3, 2)# Example of deleting the first 20 rows

my_ohlc_array = jump(my_ohlc_array, 20)# Remember, OHLC is an abbreviation of Open, High, Low, and Close and it refers to the standard historical data filedef ma(Data, lookback, close, where):

Data = adder(Data, 1)

for i in range(len(Data)):

try:

Data[i, where] = (Data[i - lookback + 1:i + 1, close].mean())

except IndexError:

pass

# Cleaning

Data = jump(Data, lookback)

return Datadef ema(Data, alpha, lookback, what, where):

alpha = alpha / (lookback + 1.0)

beta = 1 - alpha

# First value is a simple SMA

Data = ma(Data, lookback, what, where)

# Calculating first EMA

Data[lookback + 1, where] = (Data[lookback + 1, what] * alpha) + (Data[lookback, where] * beta) # Calculating the rest of EMA

for i in range(lookback + 2, len(Data)):

try:

Data[i, where] = (Data[i, what] * alpha) + (Data[i - 1, where] * beta)

except IndexError:

pass

return Datadef macd(Data, what, long_ema, short_ema, signal_ema, where):

Data = adder(Data, 1)

Data = ema(Data, 2, long_ema, what, where)

Data = ema(Data, 2, short_ema, what, where + 1)

Data[:, where + 2] = Data[:, where + 1] - Data[:, where] Data = jump(Data, long_ema)

Data = ema(Data, 2, signal_ema, where + 2, where + 3)

Data = deleter(Data, where, 2)

Data = jump(Data, signal_ema)

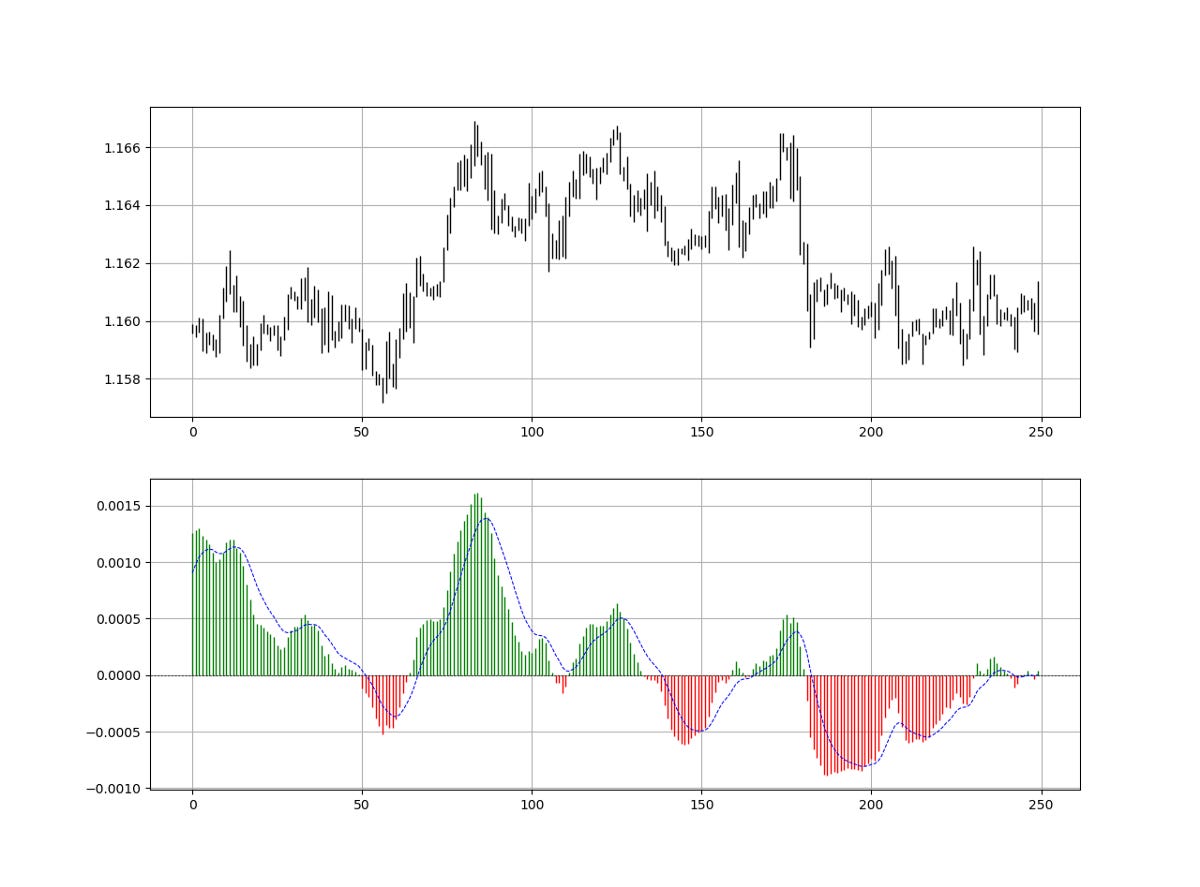

return DataAs a reminder, the MACD line is the difference between the two exponential moving averages which is plotted as histograms in green and red. The MACD signal is simply the 9-period exponential moving average of the MACD line.

The Stochastic Oscillator

The first concept to understand with the Stochastic Oscillator is normalization. This technique allows us to trap values between 0 and 1 (or 0 and 100 if we wish to multiply by 100). The concept revolves around subtracting the minimum value in a certain lookback period from the current value and dividing by the maximum value in the same lookback period minus the minimum value (the same in the nominator).

The Stochastic Oscillator seeks to find oversold and overbought zones by incorporating the highs and lows using the normalization formula as shown below:

An overbought level is an area where the market is perceived to be extremely bullish and is bound to consolidate. An oversold level is an area where market is perceived to be extremely bearish and is bound to bounce. Hence, the Stochastic Oscillator is a contrarian indicator that seeks to signal reactions of extreme movements. We will create the below function that calculates the Stochastic on an OHLC data:

def stochastic(Data, lookback, high, low, close, where, genre = 'High-Low'):

# Adding a column

Data = adder(Data, 1)

if genre == 'High-Low':

for i in range(len(Data)):

try:

Data[i, where] = (Data[i, close] - min(Data[i - lookback + 1:i + 1, low])) / (max(Data[i - lookback + 1:i + 1, high]) - min(Data[i - lookback + 1:i + 1, low]))

except ValueError:

pass

if genre == 'Normalization':

for i in range(len(Data)):

try:

Data[i, where] = (Data[i, close] - min(Data[i - lookback + 1:i + 1, close])) / (max(Data[i - lookback + 1:i + 1, close]) - min(Data[i - lookback + 1:i + 1, close]))

except ValueError:

pass

Data[:, where] = Data[:, where] * 100

Data = jump(Data, lookback) return Data

The above plot shows the EURUSD values plotted with a 70-period Stochastic Oscillator. Notice that the indicator will always be bounded between 0 and 100 due to the nature of its normalization function that traps values between the minimum and the maximum.

If you are also interested by more technical indicators and using Python to create strategies, then my best-selling book on Technical Indicators may interest you:

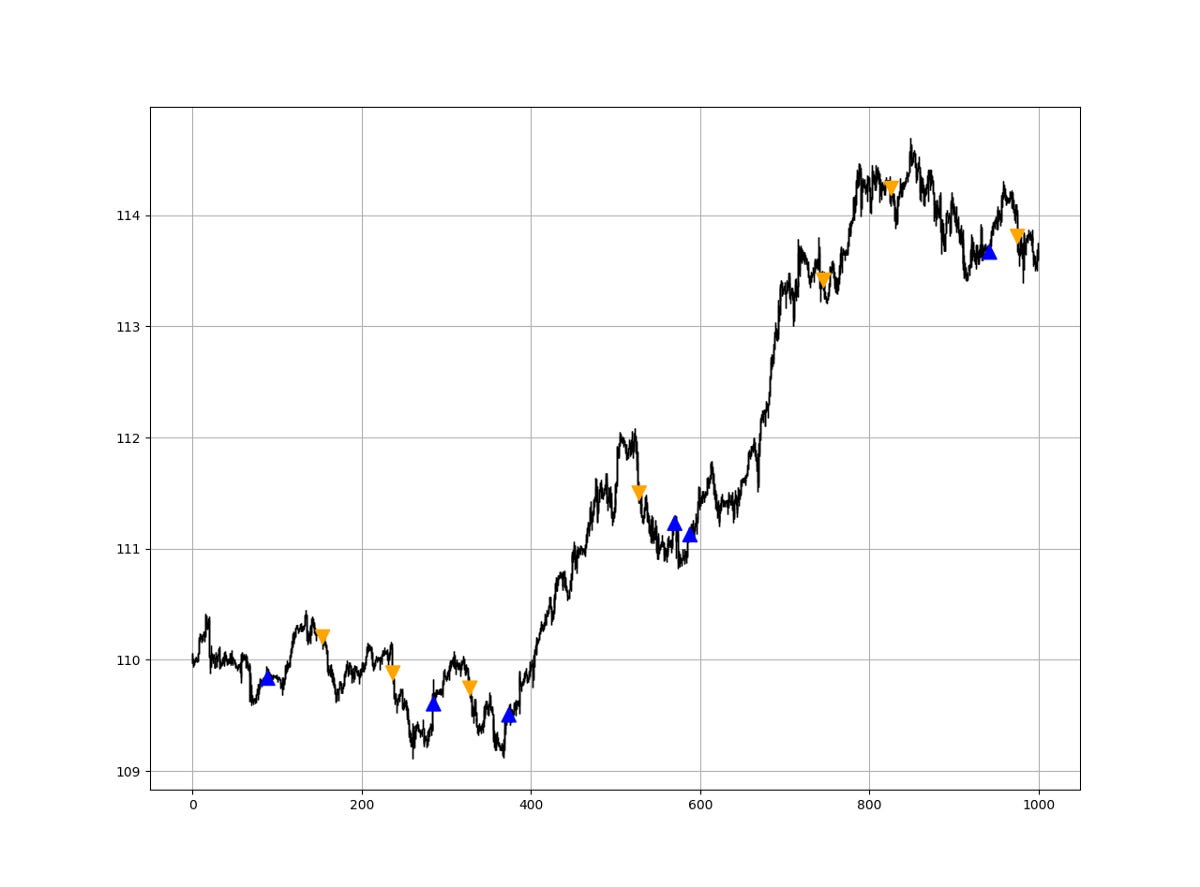

Creating the Rob Booker Reversal Indicator

The reversal indicator is an overlay indicator based on arrows created following some rules on the MACD and the Stochastic oscillators:

For a long (Buy) reversal signal, the MACD oscillator with its default parameters must surpass the zero line while the 10-period simple moving average of the 70-period Stochastic oscillator is below the lower barrier 30.

For a short (Sell) reversal signal, the MACD oscillator with its default parameters must break the zero line while the 10-period simple moving average of the 70-period Stochastic oscillator is above the upper barrier 70.

# Setting parameters

stoch_lookback = 70

lower_barrier = 30

upper_barrier = 70# Calling the 70-period Stochastic oscillator

my_data = stochastic(my_data, stoch_lookback, 1, 2, 3, 4)# Calling the 10-period moving average on the Stochastic values

my_data = ma(my_data, 10, 4, 5)# Calling the MACD function

my_data = macd(my_data, 3, 26, 12, 9, 6)

def signal(Data, stoch_col, macd_col, buy, sell):

Data = adder(Data, 10)

for i in range(len(Data)):

if Data[i, macd_col] > 0 and Data[i - 1, macd_col] < 0 and Data[i, stoch_col] < lower_barrier:

Data[i, buy] = 1

elif Data[i, macd_col] < 0 and Data[i - 1, macd_col] > 0 and Data[i, stoch_col] > upper_barrier:

Data[i, sell] = -1

return DataThe indicator can be found in some charting platforms which is already a recognition that it is accepted among the trading community. However, it is not recommended to use it alone due to its lagging nature.

Conclusion

Remember to always do your back-tests. You should always believe that other people are wrong. My indicators and style of trading may work for me but maybe not for you.

I am a firm believer of not spoon-feeding. I have learnt by doing and not by copying. You should get the idea, the function, the intuition, the conditions of the strategy, and then elaborate (an even better) one yourself so that you back-test and improve it before deciding to take it live or to eliminate it. My choice of not providing specific Back-testing results should lead the reader to explore more herself the strategy and work on it more.

To sum up, are the strategies I provide realistic? Yes, but only by optimizing the environment (robust algorithm, low costs, honest broker, proper risk management, and order management). Are the strategies provided only for the sole use of trading? No, it is to stimulate brainstorming and getting more trading ideas as we are all sick of hearing about an oversold RSI as a reason to go short or a resistance being surpassed as a reason to go long. I am trying to introduce a new field called Objective Technical Analysis where we use hard data to judge our techniques rather than rely on outdated classical methods.