Fractal Adaptive Moving Average — The Full Guide.

Coding the Fractal Adaptive Moving Average in Python.

Not all moving averages are simple to calculate. This article discusses a complex type that adapts to the market state using the Fractal Dimension Index. We will define and code it in Python.

I have just published a new book after the success of my previous one “New Technical Indicators in Python”. It features a more complete description and addition of structured trading strategies with a GitHub page dedicated to the continuously updated code. If you feel that this interests you, feel free to visit the below Amazon link, or if you prefer to buy the PDF version, you could contact me on LinkedIn.

The Concept of Moving Averages

Moving averages help us confirm and ride the trend. They are the most known technical indicator and this is because of their simplicity and their proven track record of adding value to the analyses. We can use them to find support and resistance levels, stops and targets, and to understand the underlying trend. This versatility makes them an indispensable tool in our trading arsenal.

# The function to add a number of columns inside an array

def adder(Data, times):

for i in range(1, times + 1):

new_col = np.zeros((len(Data), 1), dtype = float)

Data = np.append(Data, new_col, axis = 1)

return Data# The function to delete a number of columns starting from an index

def deleter(Data, index, times):

for i in range(1, times + 1):

Data = np.delete(Data, index, axis = 1)

return Data

# The function to delete a number of rows from the beginning

def jump(Data, jump):

Data = Data[jump:, ]

return Data# Example of adding 3 empty columns to an array

my_ohlc_array = adder(my_ohlc_array, 3)# Example of deleting the 2 columns after the column indexed at 3

my_ohlc_array = deleter(my_ohlc_array, 3, 2)# Example of deleting the first 20 rows

my_ohlc_array = jump(my_ohlc_array, 20)# Remember, OHLC is an abbreviation of Open, High, Low, and Close and it refers to the standard historical data filedef ma(Data, lookback, close, where):

Data = adder(Data, 1)

for i in range(len(Data)):

try:

Data[i, where] = (Data[i - lookback + 1:i + 1, close].mean())

except IndexError:

pass

# Cleaning

Data = jump(Data, lookback)

return DataAs the name suggests, this is your plain simple mean that is used everywhere in statistics and basically any other part in our lives. It is simply the total values of the observations divided by the number of observations. Mathematically speaking, it can be written down as:

The below states that the moving average function will be called on the array named my_data for a lookback period of 200, on the column indexed at 3 (closing prices in an OHLC array). The moving average values will then be put in the column indexed at 4 which is the one we have added using the adder function.

my_data = ma(my_data, 200, 3, 4)The aim of this article is to present a much more complex type of moving average called the Fractal Adaptive Moving Average — FRAMA. Before I introduce it, we must understand the Fractal Dimension Index before.

The Fractal Dimension Index

The index measures how irregular the time series is. When there is a strong trend going on, naturally, the market price is approaching a one-dimensional line and the Fractal Dimension Index approaches 1.0. When the market is choppy and moving sideways, the Fractal Dimension Index approaches 2.0.

def fractal_dimension(Data, lookback, high, low, close, where):

Data = adder(Data, 10)

for i in range(len(Data)):

try:

# Calculating N1

Data[i, where] = max(Data[i - (2 * lookback):i - lookback, high])

Data[i, where + 1] = min(Data[i - (2 * lookback):i - lookback, low])

Data[i, where + 2] = (Data[i, where] - Data[i, where + 1]) / lookback

# Calculating N2

Data[i, where + 3] = max(Data[i - lookback:i, high])

Data[i, where + 4] = min(Data[i - lookback:i, low])

Data[i, where + 5] = (Data[i, where + 3] - Data[i, where + 4]) / lookback

# Calculating N3

Data[i, where + 6] = max(Data[i, where], Data[i, where + 3])

Data[i, where + 7] = min(Data[i, where + 1], Data[i, where + 4])

Data[i, where + 8] = (Data[i, where + 6] - Data[i, where + 7]) / (2 * lookback)

# Calculating the Fractal Dimension Index

if Data[i, where + 2] > 0 and Data[i, where + 5] > 0 and Data[i, where + 8] > 0:

Data[i, where + 9] = (np.log(Data[i, where + 2] + Data[i, where + 5]) - np.log(Data[i, where + 8])) / np.log(2)

except ValueError:

pass

# Cleaning

Data = deleter(Data, where, 9)

Data = jump(Data, lookback * 2)

return DataAs the definition and formulas of the index are out of scope for this article, I will just provide its function which must be defined so that we code the FRAMA in the next section.

If you are also interested by more technical indicators and using Python to create strategies, then my best-selling book on Technical Indicators may interest you:

The Fractal Adaptive Moving Average

Developed by John Ehlers, the FRAMA is a special type of moving averages that uses exponential smoothing based on the current Fractal Dimension Index calculated on the price. It is also adaptive in that it is able to follow strong moves and at the same time takes into account corrections and consolidations. The first thing we need to calculate with the FRAM is the alpha factor. The alpha factor deals with the fractal smoothing part of the formula:

The above formula means that the alpha factor at any point in time equals the exponential function raised to the power of -4.6 multiplied by the current Fractal Dimension Index reading minus 1. Let us assume that we have defined the code of the FDI in the previous section and that we have an OHLC data array. To calculate a new column populated by the alpha factor, we follow this code:

# Indicator Parameters

lookback = 30# Calculating a 30-period Fractal Dimension Index

my_data = fractal_dimension(my_data, lookback, 1, 2, 3, 4)# Adding a Few Columns

my_data = adder(my_data, 1)# Calculating the alpha factor

for i in range(len(my_data)):

my_data[i, 5] = np.exp(-4.6 * (my_data[i, 4] - 1))The FRAMA is calculated following this below function.

# Calculating the First Value of FRAMA

my_data[1, 6] = (my_data[1, 5] * my_data[1, 3]) + ((1 - my_data[1, 5]) * my_data[0, 3])

# Calculating the Rest of FRAMA

for i in range(2, len(Data)):

try:

my_data[i, 6] = (my_data[i, 5] * my_data[i, 3]) + ((1 - my_data[i, 5]) * my_data[i - 1, 6])except IndexError:

pass

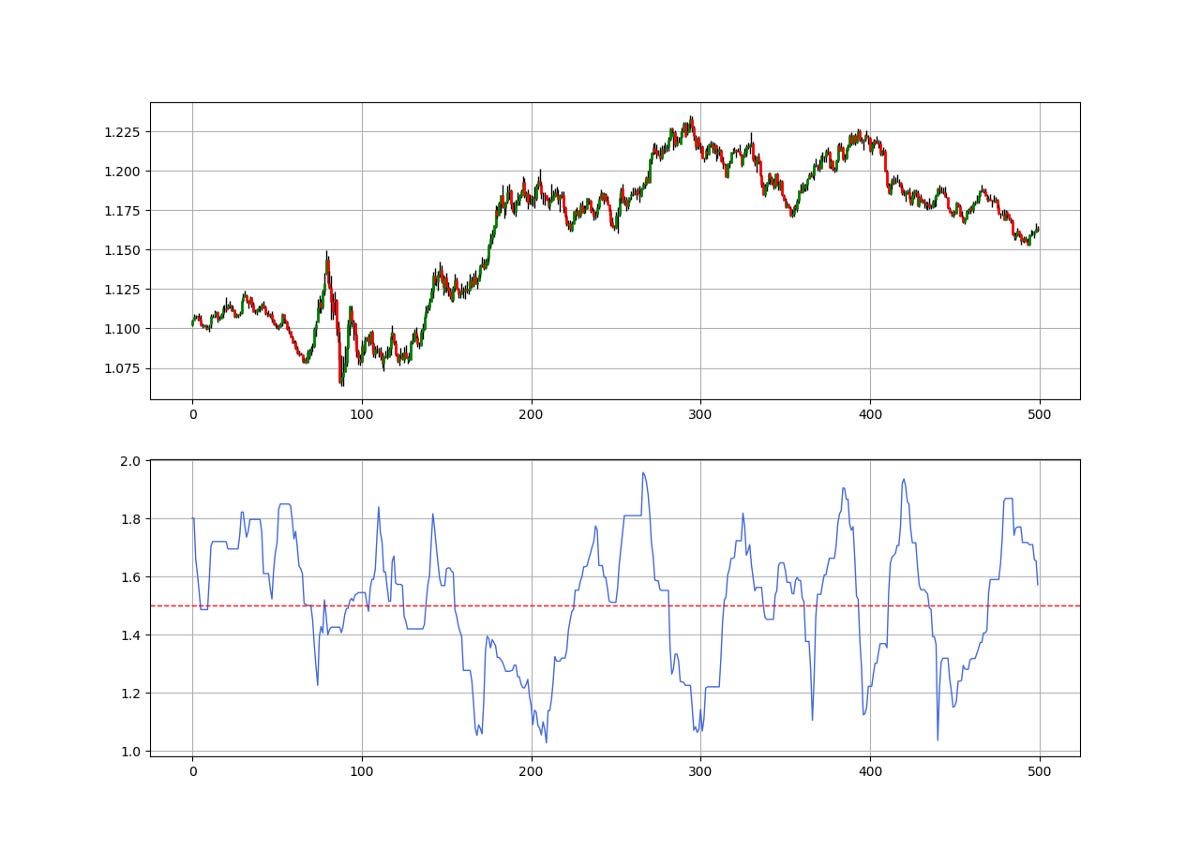

The above chart shows the EURUSD hourly values with the 50-period Fractal Adaptive Moving Average. We can notice how it adapts to the dynamic market environment. Trading strategies based on this overlay indicator are the same as any other moving average.

Conclusion

Remember to always do your back-tests. You should always believe that other people are wrong. My indicators and style of trading may work for me but maybe not for you.

I am a firm believer of not spoon-feeding. I have learnt by doing and not by copying. You should get the idea, the function, the intuition, the conditions of the strategy, and then elaborate (an even better) one yourself so that you back-test and improve it before deciding to take it live or to eliminate it. My choice of not providing specific Back-testing results should lead the reader to explore more herself the strategy and work on it more.

To sum up, are the strategies I provide realistic? Yes, but only by optimizing the environment (robust algorithm, low costs, honest broker, proper risk management, and order management). Are the strategies provided only for the sole use of trading? No, it is to stimulate brainstorming and getting more trading ideas as we are all sick of hearing about an oversold RSI as a reason to go short or a resistance being surpassed as a reason to go long. I am trying to introduce a new field called Objective Technical Analysis where we use hard data to judge our techniques rather than rely on outdated classical methods.