Detecting Market Regime With the Momentum Ratio Technique.

A Visual Way of Using Technical Indicators to Understand the Current Regime.

Color-coding charts can be helpful to determine the market’s state when we want to take a quick glance at the charts. True we might be able to determine the trend visually or by using moving averages, but we can also use other indicators and transform the chart so that it reflects the indicator’s values. This article will discuss how to do that. The aim is to be able to produce multiple charts at the same time with a color code that shows our conditions.

I have just published a new book after the success of my previous one “New Technical Indicators in Python”. It features a more complete description and addition of structured trading strategies with a GitHub page dedicated to the continuously updated code. If you feel that this interests you, feel free to visit the below link, or if you prefer to buy the PDF version, you could contact me on LinkedIn.

Fetching Historical OHLC Data

One of the most famous trading platforms in the retail community is the MetaTrader5 software. It is a powerful tool that comes with its own programming language and its huge online community support. It also offers the possibility to export its historical short-term and long-term FX data.

The first thing we need to do is to simply download the platform from the official website. Then, after creating the demo account, we are ready to import the library in Python that allows to import the OHLC data from MetaTrader5.

A library is a group of structured functions that can be imported into our Python interpreter from where we can call and use the ones we want.

The easiest way to install the MetaTrader5 library is to go to the Python prompt on our computer and type:

pip install MetaTrader5This should install the library in our local Python. Now, we want to import it to the Python interpreter (such as Pycharm or SPYDER) so that we can use it. Let us actually import all the libraries we will be using for this:

import datetime # Date acquiring

import pytz # Time zone management

import pandas as pd # Mostly for Data frame manipulation

import MetaTrader5 as mt5 # Importing OHLC data

import matplotlib.pyplot as plt # Plotting charts

import numpy as np # Mostly for array manipulationAnything that comes after “as” is a shortcut. The plt shortcut is there so that each time we want to call a function from that library we do not have to type the full matplotlib.pyplot statement.

The official documentation for the Metatrader5 libary can be found here.

The first thing we can do is to select which time frame we want to import. Let us suppose that there are only two time frames, the 30-minute and the hourly bars. We can therefore create variables that hold the statement to tell the MetaTrader5 library which time frame we want.

# Choosing the 30-minute time frame

frame_M30 = mt5.TIMEFRAME_M30

# Choosing the hourly time frame

frame_H1 = mt5.TIMEFRAME_H1Then, by staying in the spirit of importing variables, we can define the variable that states what date is it now. This helps the algorithm know the stopping date of the import. We can do this by the simple line of code below.

# Defining the variable now to give out the current date

now = datetime.datetime.now()Note that these code snippets are better used chronologically, hence, I encourage you to copy them in order and then execute them one by one so that you understand the evolution of what you are doing. The below is a function that holds which assets we want. Generally, I use 10 or more but for simplicity, let us consider that there are only two currency pairs: EURUSD and USDCHF.

def asset_list(asset_set):

if asset_set == 'FX':

assets = ['EURUSD', 'USDCHF']

return assetsNow, with the key function that gets us the OHLC data. The below establishes a connection to MetaTrader5, applies the current date, and extracts the needed data. Notice the arguments year, month, and day. These will be filled by us to select from when do we want the data to start. Note, I have inputed Europe/Paris as my time zone, you should use your time zone to get more accurate data.

def get_quotes(time_frame, year = 2005, month = 1, day = 1, asset = "EURUSD"):

# Establish connection to MetaTrader 5

if not mt5.initialize():

print("initialize() failed, error code =", mt5.last_error())

quit()

timezone = pytz.timezone("Europe/Paris")

utc_from = datetime.datetime(year, month, day, tzinfo = timezone)

utc_to = datetime.datetime(now.year, now.month, now.day + 1, tzinfo = timezone)

rates = mt5.copy_rates_range(asset, time_frame, utc_from, utc_to)

rates_frame = pd.DataFrame(rates)

return rates_frameAnd finally, the last function we will use is the one that uses the below get_quotes function and then cleans the results so that we have a nice array. We have selected data since January 2019 as shown below.

def mass_import(asset, horizon):

if horizon == 'M30':

data = get_quotes(frame_M30, 2019, 1, 1, asset = assets[asset])

data = data.iloc[:, 1:5].values

data = data.round(decimals = 5)

return dataFinally, we are done building the blocks necessary to import the data. To import EURUSD OHLC historical data, we simply use the below code line:

# Choosing the horizon

horizon = 'M30'

# Creating an array called EURUSD having M30 data since 2019

EURUSD = mass_import(0, horizon)And voila, now we have the EURUSD OHLC data from 2019.

The Market’s Regime

The market’s regime is its current state and can be divided into:

Bullish trend: The market has a tendency to make higher highs meaning that the aggregate direction is upwards.

Sideways: The market has a tendency to to range while remaining within established zones.

Bearish trend: The market has a tendency to make lower lows meaning that the aggregate direction is downwards.

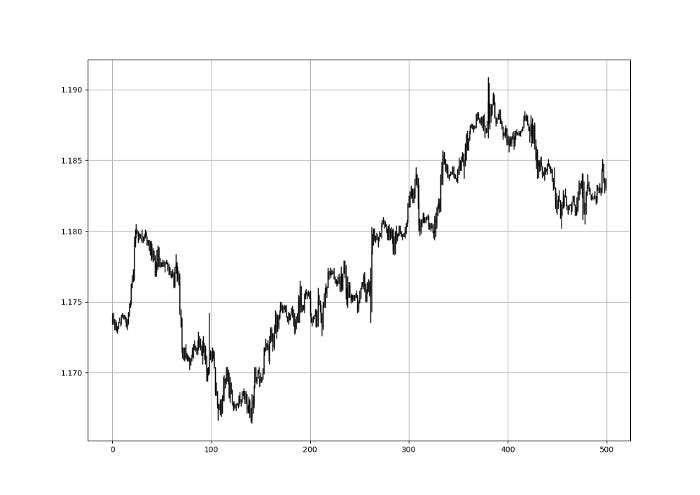

Many tools attempt to detect the trend and most of them do give the answer but we can not really say we can predict the next state. The best way to solve this issue is to assume that the current state will continue and trade any reactions, preferably in the direction of the trend. For example, if the EURUSD is above its moving average and shaping higher highs, then it makes sense to wait for dips before buying and assuming that the bullish state will continue, also known as a trend-following strategy.

The above chart shows the EURUSD’s hourly values where the market trended upwards for a while before reversing.

The Momentum Ratio Technique

The technique uses two Relative Strength Indices where we use the ratio between the short-term RSI and the long-term RSI to understand the current momentum.

The RSI is without a doubt the most famous momentum indicator out there, and this is to be expected as it has many strengths especially in ranging markets. It is also bounded between 0 and 100 which makes it easier to interpret. Also, the fact that it is famous, contributes to its potential.

This is because the more traders and portfolio managers look at the RSI, the more people will react based on its signals and this in turn can push market prices. Of course, we cannot prove this idea, but it is intuitive as one of the basis of Technical Analysis is that it is self-fulfilling.

The RSI is calculated using a rather simple way. We first start by taking price differences of one period. This means that we have to subtract every closing price from the one before it. Then, we will calculate the smoothed average of the positive differences and divide it by the smoothed average of the negative differences. The last calculation gives us the Relative Strength which is then used in the RSI formula to be transformed into a measure between 0 and 100.

To calculate the Relative Strength Index, we need an OHLC array (not a data frame). This means that we will be looking at an array of 4 columns. The function for the Relative Strength Index is therefore:

# The function to add a number of columns inside an array

def adder(Data, times):

for i in range(1, times + 1):

new_col = np.zeros((len(Data), 1), dtype = float)

Data = np.append(Data, new_col, axis = 1)

return Data

# The function to delete a number of columns starting from an index

def deleter(Data, index, times):

for i in range(1, times + 1):

Data = np.delete(Data, index, axis = 1)

return Data

# The function to delete a number of rows from the beginning

def jump(Data, jump):

Data = Data[jump:, ]

return Data

# Example of adding 3 empty columns to an array

my_ohlc_array = adder(my_ohlc_array, 3)

# Example of deleting the 2 columns after the column indexed at 3

my_ohlc_array = deleter(my_ohlc_array, 3, 2)

# Example of deleting the first 20 rows

my_ohlc_array = jump(my_ohlc_array, 20)

# Remember, OHLC is an abbreviation of Open, High, Low, and Close and it refers to the standard historical data file

def ma(Data, lookback, close, where):

Data = adder(Data, 1)

for i in range(len(Data)):

try:

Data[i, where] = (Data[i - lookback + 1:i + 1, close].mean())

except IndexError:

pass

# Cleaning

Data = jump(Data, lookback)

return Data

def ema(Data, alpha, lookback, what, where):

alpha = alpha / (lookback + 1.0)

beta = 1 - alpha

# First value is a simple SMA

Data = ma(Data, lookback, what, where)

# Calculating first EMA

Data[lookback + 1, where] = (Data[lookback + 1, what] * alpha) + (Data[lookback, where] * beta)

# Calculating the rest of EMA

for i in range(lookback + 2, len(Data)):

try:

Data[i, where] = (Data[i, what] * alpha) + (Data[i - 1, where] * beta)

except IndexError:

pass

return Data

def rsi(Data, lookback, close, where, width = 1, genre = 'Smoothed'):

# Adding a few columns

Data = adder(Data, 7)

# Calculating Differences

for i in range(len(Data)):

Data[i, where] = Data[i, close] - Data[i - width, close]

# Calculating the Up and Down absolute values

for i in range(len(Data)):

if Data[i, where] > 0:

Data[i, where + 1] = Data[i, where]

elif Data[i, where] < 0:

Data[i, where + 2] = abs(Data[i, where])

# Calculating the Smoothed Moving Average on Up and Down

absolute values

if genre == 'Smoothed':

lookback = (lookback * 2) - 1 # From exponential to smoothed

Data = ema(Data, 2, lookback, where + 1, where + 3)

Data = ema(Data, 2, lookback, where + 2, where + 4)

if genre == 'Simple':

Data = ma(Data, lookback, where + 1, where + 3)

Data = ma(Data, lookback, where + 2, where + 4)

# Calculating the Relative Strength

Data[:, where + 5] = Data[:, where + 3] / Data[:, where + 4]

# Calculate the Relative Strength Index

Data[:, where + 6] = (100 - (100 / (1 + Data[:, where + 5])))

# Cleaning

Data = deleter(Data, where, 6)

Data = jump(Data, lookback)

return Data

The formula for the technique we will be using is:

We will use the following intuition:

Whenever the 5-period RSI is above the 13-period RSI, a bullish momentum is in place.

Whenever the 5-period RSI is below the 13-period RSI, a bearish momentum is in place.

lookback_long = 13

lookback_short = 5

my_data = adder(my_data, 10)

my_data = rsi(my_data, lookback_short, 3, 4)

my_data = rsi(my_data, lookback_long, 3, 5)

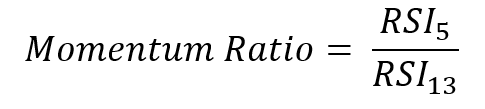

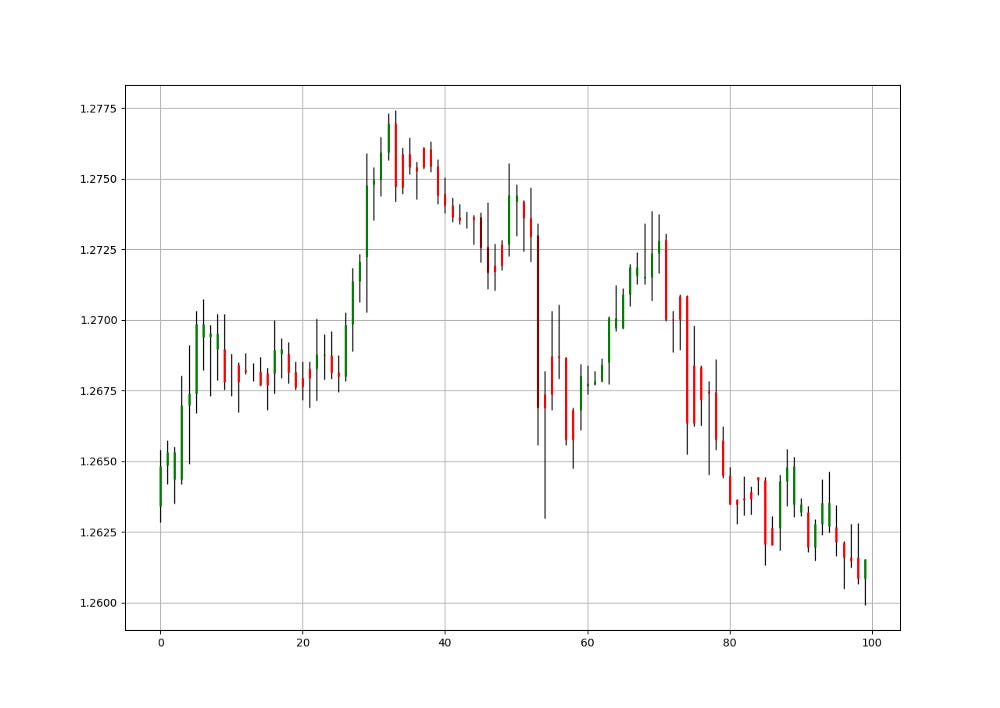

my_data[:, 6] = my_data[:, 4] / my_data[:, 5]Let us look at the below candlestick chart on the USDCAD and compare it with the following color-coded chart based on the Momentum ratio technique.

The color codes are as follows:

Sea green: Whenever the ratio is at 1.5 or higher, signifying a strong bullish momentum but also a risk of overbought.

Green: Whenever the ratio is greater than 1 but lower than 1.5, signifying a bullish momentum.

Red: Whenever the ratio is less than 1 but greater than 0.5, signifying a bearish momentum.

Dark red: Whenever the ratio is at 0.5 or lower, signifying a strong bearish momentum but also a risk of oversold.

def ohlc_plot_candles(Data, window):

Chosen = Data[-window:, ]

for i in range(len(Chosen)):

if Chosen[i, 6] > 1 and Chosen[i, 6] < 1.5:

plt.vlines(x = i, ymin = Chosen[i, 2], ymax = Chosen[i, 1], color = 'black', linewidth = 0.5)

color_chosen = 'green'

plt.vlines(x = i, ymin = Chosen[i, 0], ymax = Chosen[i, 3], color = color_chosen, linewidth = 1.5)

if Chosen[i, 6] < 1 and Chosen[i, 6] > 0.5:

plt.vlines(x = i, ymin = Chosen[i, 2], ymax = Chosen[i, 1], color = 'black', linewidth = 0.5)

color_chosen = 'red'

plt.vlines(x = i, ymin = Chosen[i, 3], ymax = Chosen[i, 0], color = color_chosen, linewidth = 1.5)

if Chosen[i, 6] < 0.5:

plt.vlines(x = i, ymin = Chosen[i, 2], ymax = Chosen[i, 1], color = 'black', linewidth = 0.5)

color_chosen = 'darkred'

plt.vlines(x = i, ymin = Chosen[i, 3], ymax = Chosen[i, 0], color = color_chosen, linewidth = 1.5)

if Chosen[i, 6] > 1.5:

plt.vlines(x = i, ymin = Chosen[i, 2], ymax = Chosen[i, 1], color = 'black', linewidth = 0.5)

color_chosen = 'seagreen'

plt.vlines(x = i, ymin = Chosen[i, 3], ymax = Chosen[i, 0], color = color_chosen, linewidth = 1.5)

plt.grid()

The above charts showed more smoothing and regime filtering that can help us with our trading decisions. The periods of the RSI can be tweaked and optimized. Also trading strategies can be formed around the values of this ratio.

One such example of a trading strategy would be to take the bullish signals from independent RSI’s while the Momentum technique is above 1.0. Similarly, we can take the bearish signals from independent RSI’s while the Momentum technique is less than 1.0.

If you are also interested by more technical indicators and using Python to create strategies, then my best-selling book on Technical Indicators may interest you:

Conclusion

Remember to always do your back-tests. You should always believe that other people are wrong. My indicators and style of trading may work for me but maybe not for you.

I am a firm believer of not spoon-feeding. I have learnt by doing and not by copying. You should get the idea, the function, the intuition, the conditions of the strategy, and then elaborate (an even better) one yourself so that you back-test and improve it before deciding to take it live or to eliminate it. My choice of not providing specific Back-testing results should lead the reader to explore more herself the strategy and work on it more.

To sum up, are the strategies I provide realistic? Yes, but only by optimizing the environment (robust algorithm, low costs, honest broker, proper risk management, and order management). Are the strategies provided only for the sole use of trading? No, it is to stimulate brainstorming and getting more trading ideas as we are all sick of hearing about an oversold RSI as a reason to go short or a resistance being surpassed as a reason to go long. I am trying to introduce a new field called Objective Technical Analysis where we use hard data to judge our techniques rather than rely on outdated classical methods.